[H1] The CCS Carbon Credits Market: A Technical and Commercial Primer for Industrial Stakeholders

Introduction: The Evolving Value Proposition of Carbon Capture

The global imperative to achieve net-zero emissions is fundamentally reshaping the economics of heavy industry and the energy sector. For operators of industrial plants, power generation facilities, and upstream hydrocarbon assets, Carbon Capture and Storage (CCS) has transitioned from a theoretical mitigation option to a critical operational and strategic consideration. Central to this shift is the emerging and complex CCS carbon credits market, a financial mechanism that can transform captured CO₂ from a cost center into a potential revenue stream. This market directly intersects with engineering feasibility, project financing, and corporate ESG mandates. For engineers, project managers, and executives, understanding the nuances of this market is no longer just about compliance; it’s about asset valuation, competitive advantage, and strategic resilience in a decarbonizing world. This article provides a technically grounded and commercially focused analysis of the CCS carbon credits landscape, tailored for industrial decision-makers.

Understanding Carbon Credit Fundamentals for CCS

Carbon credits, or carbon offsets, represent a standardized unit—typically one metric tonne of carbon dioxide equivalent (CO₂e)—that is reduced, removed, or avoided. The CCS carbon credits market specifically deals with credits generated from the permanent geological sequestration of CO₂ that would otherwise be released into the atmosphere.

Credit Typology: Avoidance vs. Removal

This is a critical technical and commercial distinction. Most existing compliance markets (e.g., EU ETS) have historically traded avoidance credits (e.g., from switching to a less carbon-intensive fuel). CCS, particularly from industrial point sources or via Direct Air Capture (DAC), generates removal credits. Removal credits are increasingly viewed as higher integrity and are expected to command a premium, as they actively reduce atmospheric CO₂ concentrations. For an LNG facility or a cement plant, the credits generated from capturing process emissions are removal credits, altering the core project economics.

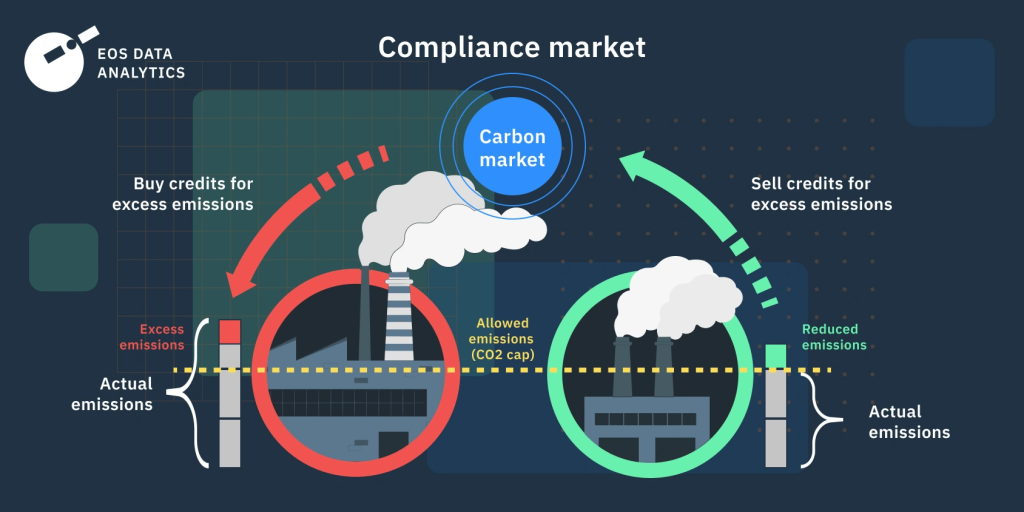

Key Market Segments: Compliance vs. Voluntary

Compliance Markets: Government-mandated systems (e.g., California’s Low-Carbon Fuel Standard, UK ETS) where emitters must surrender allowances. CCS can generate credits for use within these schemes, but methodologies are often stringent and geographically specific.

Voluntary Carbon Market (VCM): Driven by corporate net-zero pledges. Companies buy CCS-derived credits to offset their residual emissions. The VCM for CCS is rapidly evolving, with a strong emphasis on durability, measurement, and additionality.

The Value Chain of a CCS Credit: From Pore Space to Portfolio

The generation of a verifiable carbon credit from a CCS project is a multi-stage, technically intensive process.

1. Capture & Quantification

The foundation lies in accurate measurement. This involves continuous emission monitoring systems (CEMS) at the capture facility. Engineering standards from ISO (ISO 27917:2017 for CCS terminology) and the IPCC provide guidelines for calculating captured volumes. Uncertainty margins must be rigorously defined, as they directly impact the number of credits issued.

2. Transportation & Injection

The secure transport (via pipeline or ship) and injection into a certified geological storage site (e.g., depleted offshore reservoir, saline aquifer) must be meticulously documented. Subsea engineering protocols, well integrity management (following API and ISO standards), and reservoir surveillance plans are not just operational necessities but credit verification prerequisites.

3. Monitoring, Reporting, and Verification (MRV)

This is the cornerstone of market integrity. A robust MRV plan, often required for 30+ years post-injection, must demonstrate permanent containment. Technologies include:

4D seismic surveys for plume tracking.

Downhole pressure and temperature monitoring.

Atmospheric and soil gas monitoring for leak detection.

Independent third-party verification against a recognized carbon standard (e.g., Verra, American Carbon Registry, Gold Standard) is mandatory for credit issuance.

4. Registry and Retirement

Once verified, credits are issued into a digital registry. When a buyer uses a credit to offset an emission, it is “retired” permanently to prevent double-counting. Blockchain and other digital MRV platforms are emerging to enhance transparency in this phase.

Engineering and Operational Drivers of Credit Value

Not all CCS credits are equal. Their value in the CCS carbon credits market is heavily influenced by project-specific engineering and operational factors.

Storage Site Integrity and Durability

The perceived permanence of storage (typically targeting >99% retention over 1,000 years) is paramount. Credits from projects using well-characterized, sealed saline formations or depleted fields with extensive historical data (common in offshore oil & gas regions) may be de-risked and more valuable. Detailed site characterization, including geomechanical modeling and fault seal analysis, is crucial.

Measurement Uncertainty and Buffer Pools

Carbon standards mandate holding a portion of generated credits in a “buffer pool” as insurance against any future reversal (leakage). Projects with superior MRV technology, lower measurement uncertainty, and exceptional site integrity may be required to contribute a smaller percentage to this buffer, thereby monetizing a higher proportion of their captured CO₂.

Project Additionality and Benchmarking

A key tenet, especially in the VCM, is that the CCS project would not have happened without the carbon credit revenue. This involves financial additionality tests and benchmarking against a “business-as-usual” scenario. For a retrofit on a legacy gas processing platform, this case is easier to make than for a new-build facility where capture is already mandated.

Commercial Risks and Market Constraints

While the potential is significant, the CCS carbon credits market presents substantial commercial and operational hurdles.

Price Volatility and Long-Term Investment

Current voluntary carbon prices are volatile and, for many industrial CCS projects, still below the full cost of capture, transport, and storage. Financing a $500 million+ CCS cluster requires long-term offtake agreements or a firm price floor, which the nascent market often cannot yet provide. This creates a “chicken-and-egg” financing dilemma.

Regulatory and Policy Uncertainty

The regulatory framework for CCS ownership, long-term liability for stored CO₂, and the treatment of carbon credits is still evolving in many jurisdictions. Clarity on who owns the pore space, liability transfer post-closure, and how CCS credits will be treated in future compliance schemes is critical for final investment decisions (FID).

Cross-Border Logistics and Standards

Capturing CO₂ in one country, shipping it via subsea pipeline to another for storage, and then generating a credit usable in a third market involves immense legal, regulatory, and standards alignment. Issues of chain of custody, international accounting under the Paris Agreement (Article 6), and liability are complex.

The Future Outlook: Integration and Industrial Scale

The trajectory of the CCS carbon credits market is towards greater rigor, integration, and scale.

The Rise of Industrial Hubs and Clusters

Economies of scale are driving the development of industrial CCS hubs, Carbon Capture and Storage, where multiple emitters share transportation and storage infrastructure (e.g., the Northern Lights project in Norway, Gulf Coast hubs in the US). This reduces unit costs and creates a standardized, large-volume credit supply, making the market more liquid and attractive to investors.

Technology Integration: DACCS and BECCS

The market will expand beyond point-source capture to include Direct Air Capture with Storage (DACCS) and Bioenergy with CCS (BECCS). DACCS generates purely removal credits, while BECCS can generate net-negative credits. These technologies have different cost structures and credit profiles but will broaden the market.

Regulatory Convergence and Quality Mandates

Expect a forceful shift towards high-integrity credits. Initiatives like the ICVCM’s Core Carbon Principles and potential US/EU regulations on offset quality will marginalize low-quality credits. This will benefit engineered, geologically stored CCS solutions with robust MRV, solidifying their role as a premium asset class.

Frequently Asked Questions

Q1: For an offshore operator, what are the key differences between storing CO₂ for Enhanced Oil Recovery (EOR) and generating carbon credits?

The objectives and accounting differ fundamentally. EOR uses CO₂ as an operational fluid to increase hydrocarbon production, with a portion of the CO₂ remaining sequestered. The carbon accounting is complex, and credits, if generated, must account for the emissions from the additional oil produced. Dedicated geological storage for carbon credits has no production objective—its sole purpose is permanent sequestration. The MRV requirements for credit generation are typically more stringent and singularly focused on proving permanent containment.

Q2: How does the “permanence” requirement of carbon credits (often 100+ years) affect long-term liability for the operator?

This is a critical commercial and legal issue. During the operational and initial post-closure monitoring phase, liability typically rests with the project operator. Many jurisdictions are developing frameworks for liability transfer to the state after a demonstrable period of safe closure (e.g., after 20-30 years of post-injection monitoring showing stability). The specific terms are project-defined and must be contractually secured before FID, as they drastically impact the project’s risk profile and financing.

Q3: Can a company claim both a carbon credit and a government tax incentive (like 45Q in the US) for the same tonne of CO₂?

Generally, no. This is known as “double-dipping” and is prohibited. The principle is that only one financial mechanism should be claimed per tonne of CO₂ sequestered. A project must elect to either receive the tax credit or generate and sell a carbon credit. The commercial decision hinges on comparing the guaranteed value of the tax credit against the projected, but potentially higher, market price of the carbon credit, factoring in all transaction and verification costs.

Q4: What is the role of Class VI wells (in the US) or similar storage permits in carbon credit generation?

A granted Class VI Underground Injection Control (UIC) permit from the EPA (or its equivalent, like a Storage Permit under the EU’s CCS Directive) is not just an operational license—it is a primary signal of credit quality. The rigorous permitting process, which includes extensive site characterization, modeling, and MRV planning, de-risks the project in the eyes of credit verifiers and buyers. Credits from permitted geologic storage sites are considered more bankable and will likely command a market premium.

Q5: How are maritime and subsea transport of CO₂ factored into the carbon credit lifecycle analysis?

The full lifecycle emissions of the CCS chain must be net-negative. The emissions from the energy used for liquefaction, pumping, and shipping of CO₂ (e.g., by a dedicated CO₂ carrier) are meticulously calculated and deducted from the total tonnes sequestered. Only the net amount is eligible for credit generation. This makes the energy efficiency of compression, pipeline hydraulics, and vessel design direct drivers of the project’s credit yield.

The CCS carbon credits market is maturing from a speculative concept into a tangible, albeit complex, component of industrial project finance. For asset owners in the energy and heavy industry sectors, engagement with this market is increasingly non-optional. Success requires a deeply integrated approach, where subsurface engineers, process designers, commercial managers, and legal counsel collaborate from the project’s inception. The future will reward projects that prioritize verifiable storage integrity, transparent MRV, and seamless integration into emerging industrial clusters. While significant challenges around pricing, regulation, and liability persist, the directional shift is clear: carbon management is becoming a core industrial competency, and the ability to navigate the carbon credits marketplace will be a key differentiator for resilient, low-carbon industrial enterprises. The time for strategic evaluation and technical preparation is now.